What is Kisan Credit Card? How to Avail the Scheme

The Kisan Credit Card (KCC) scheme is one of the most important agricultural credit initiatives in India. It was introduced in 1998 by the Reserve Bank of India and National Bank for Agriculture and Rural Development to provide farmers with timely and affordable credit for agricultural needs.

Before the introduction of KCC, farmers often depended on informal moneylenders who charged very high interest rates. The KCC scheme was designed to simplify the process of obtaining agricultural loans and ensure that farmers have easy access to working capital for crop production and related activities.

Over the years, the scheme has been expanded and modernized, including linking KCC with the Pradhan Mantri Jan Dhan Yojana and introducing debit card–enabled credit facilities.

Objectives of the Kisan Credit Card Scheme

The main objectives of the KCC scheme are:

- Provide timely credit to farmers for agricultural operations.

- Reduce dependence on moneylenders in rural areas.

- Simplify loan procedures for crop production and allied activities.

- Ensure financial inclusion of farmers in the formal banking system.

- Promote agricultural productivity by providing adequate working capital.

Features of the KCC Scheme

The Kisan Credit Card scheme has several important features that make it beneficial for farmers.

1. Flexible Credit Limit

Farmers receive a revolving credit limit based on:

- Landholding size

- Cropping pattern

- Cost of cultivation

2. Multi-purpose Use

The loan can be used for:

- Crop cultivation

- Purchase of seeds, fertilizers, pesticides

- Farm machinery repair

- Post-harvest expenses

- Household consumption (limited)

3. Interest Subsidy

Farmers benefit from government interest subsidies.

For example, short-term crop loans are often available at 4% effective interest rate if repayment is made on time.

4. Debit Card Facility

Many banks issue RuPay Kisan Cards, which allow farmers to withdraw money from ATMs and make digital payments.

5. Insurance Coverage

KCC holders may also be covered under crop insurance schemes such as Pradhan Mantri Fasal Bima Yojana.

6. Validity Period

KCC accounts generally have a validity of five years, subject to annual review.

Eligible Beneficiaries

The following categories are eligible for the KCC scheme:

- Individual farmers (owner cultivators)

- Tenant farmers and sharecroppers

- Self-Help Groups (SHGs) or Joint Liability Groups (JLGs) of farmers

- Farmers involved in allied activities such as:

- Dairy farming

- Fisheries

- Poultry farming

- Animal husbandry

The scheme has been expanded to include farmers engaged in livestock and fisheries activities.

Loan Limit under KCC

The loan amount depends on the farmer’s requirements and landholding.

Typical credit limits include:

| Category | Credit Limit |

|---|---|

| Small farmers | Up to ₹50,000 |

| Medium farmers | ₹50,000 – ₹3 lakh |

| Larger farmers | Above ₹3 lakh depending on cultivation cost |

Loans up to ₹1.6 lakh generally do not require collateral security.

Documents Required

To apply for a Kisan Credit Card, farmers usually need:

- Identity proof (Aadhaar card, voter ID, etc.)

- Address proof

- Land ownership documents or cultivation certificate

- Passport-size photographs

- Bank account details

Banks may require additional documents depending on the loan amount.

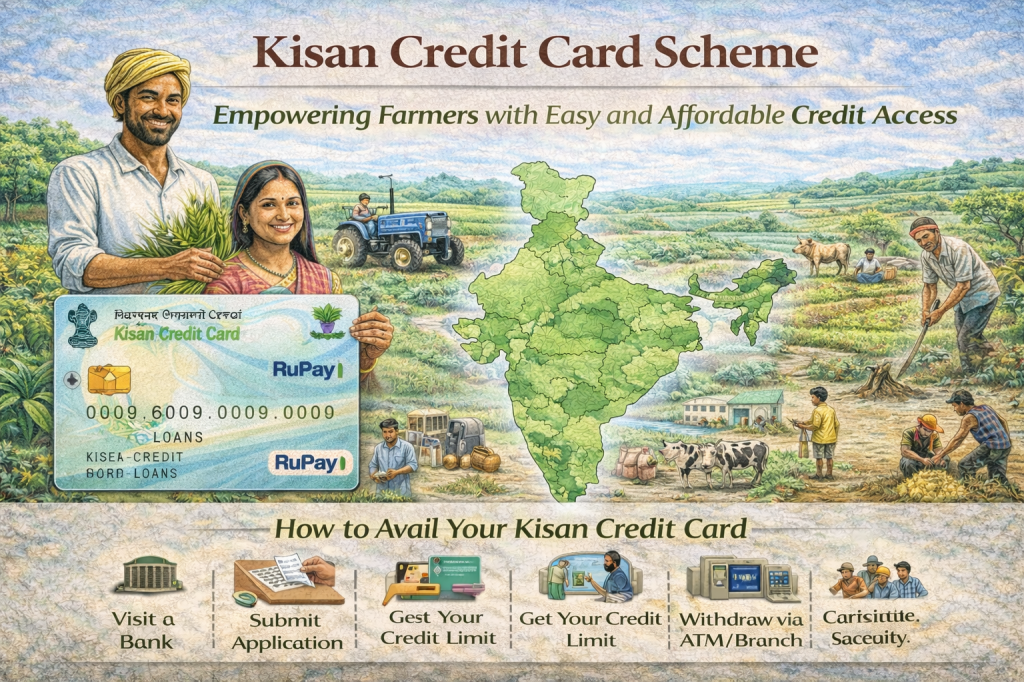

How to Avail the Kisan Credit Card (Application Process)

Farmers can obtain a KCC through the following steps:

Step 1: Visit a Bank

Farmers can apply at:

- State Bank of India

- Punjab National Bank

- Bank of Baroda

- Regional Rural Banks (RRBs)

- Cooperative Banks

Step 2: Fill the Application Form

The farmer fills out the KCC application form with details about landholding, crops grown, and credit requirement.

Step 3: Submit Required Documents

Attach identity proof, land records, and photographs.

Step 4: Verification by the Bank

The bank verifies:

- Land ownership or cultivation status

- Credit history

- Crop pattern and loan requirement

Step 5: Sanction of Loan

Once approved, the bank issues a Kisan Credit Card with a credit limit.

Step 6: Use of Credit

The farmer can withdraw funds using:

- Bank branch

- ATM using RuPay KCC card

- Digital payment systems

Benefits of the KCC Scheme

The KCC scheme offers numerous advantages to farmers:

1. Easy Access to Credit

Farmers can obtain credit quickly without lengthy procedures.

2. Lower Interest Rates

Government subsidies reduce borrowing costs.

3. Flexible Repayment

Repayment is generally linked to harvest cycles, making it convenient for farmers.

4. Reduced Dependence on Moneylenders

The scheme encourages farmers to use formal banking channels.

5. Financial Inclusion

It integrates farmers into the banking system and promotes digital payments.

Achievements of the KCC Scheme

The Kisan Credit Card scheme has made a significant impact on rural credit delivery.

- Millions of farmers across India have received KCC cards.

- The scheme has strengthened the agricultural credit system.

- It has helped improve crop production and rural livelihoods.

The government continues to expand KCC coverage, especially among small and marginal farmers.

Challenges of the KCC Scheme

Despite its success, the scheme faces some challenges:

- Limited awareness among farmers in remote areas

- Difficulties for tenant farmers without land documents

- Delays in loan approval in some banks

- Need for better digital access in rural areas

Efforts are being made to address these issues through financial literacy programs and simplified procedures.

Conclusion

The Kisan Credit Card scheme is a crucial initiative for strengthening agricultural credit in India. By providing easy, affordable, and flexible loans to farmers, the scheme has helped improve agricultural productivity and reduce dependence on informal lenders. The KCC programme will continue to expand. Technological improvements will also occur. It will remain a key instrument for promoting sustainable agricultural development. It will enhance the livelihoods of farmers across the country.

Leave a comment