1. Overview & Background

- MISS is a Central Sector Scheme under India’s Ministry of Agriculture & Farmers’ Welfare (MoA&FW). It aims to make short-term credit affordable for farmers.

- The scheme has its origins in the earlier interest subvention initiatives from around 2006-07. These initiatives aimed to reduce the cost of agricultural loans, especially through the Kisan Credit Card (KCC) Scheme.

- The scheme was recently extended for FY 2025-26, maintaining key subsidy parameters. (Press Information Bureau)

2. Objectives

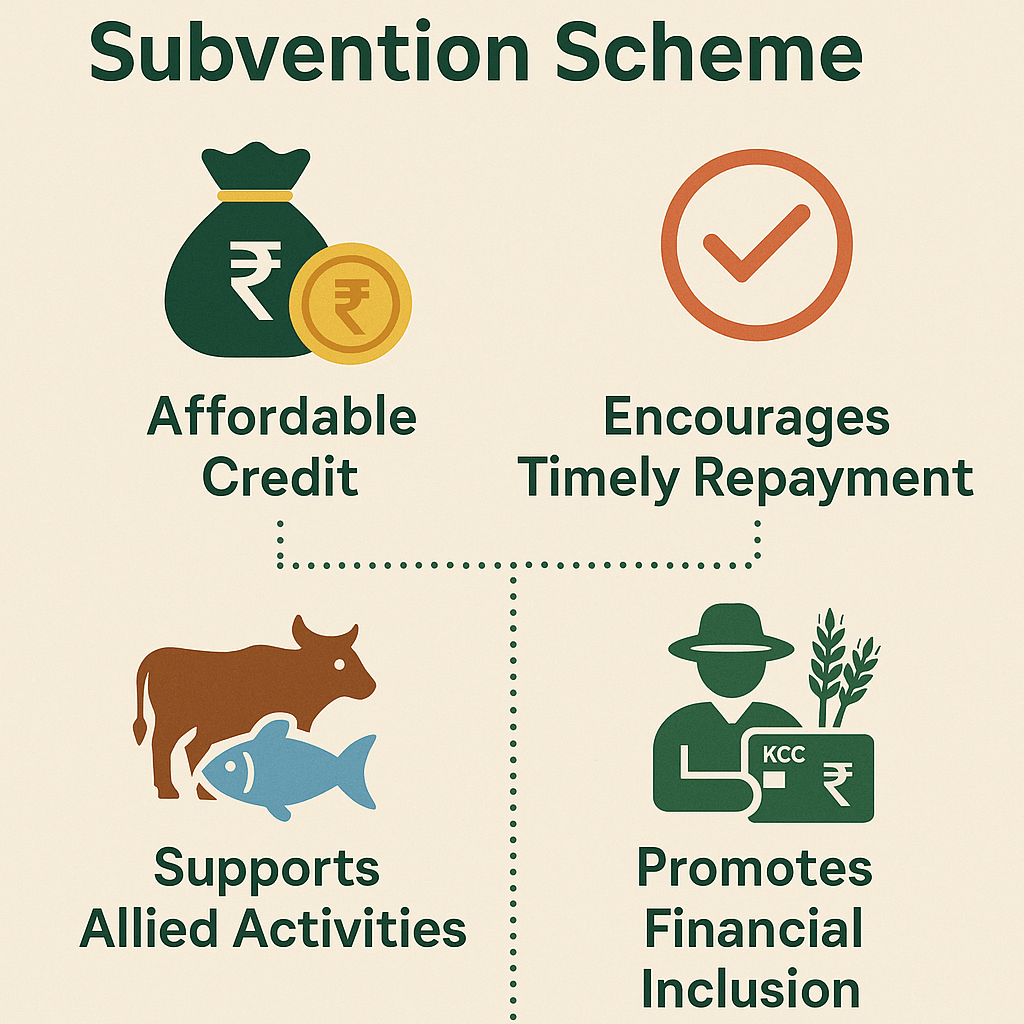

The primary goals of MISS include:

- Ensuring availability of short-term agricultural credit to farmers at reduced interest rates.

- Encouraging prompt repayment of loans (thus reducing default risk and improving institutional credit flow).

- Supporting allied agricultural activities (animal husbandry, fisheries) through the credit system.

- Enhancing financial inclusion of small and marginal farmers by making institutional credit more accessible and less costly.

3. Key Features / Scheme Design

Here’s a table summarizing the core parameters of MISS:

| Feature | Details |

|---|---|

| Loan Type | Short-term crop loans via Kisan Credit Card (KCC) and allied activities |

| Maximum Loan Amount | Up to ₹ 3 lakh for crop loans under KCC. (Press Information Bureau) For animal husbandry/fisheries “up to ₹ 2 lakh” benefit eligibility. |

| Interest Rate to Farmers | Standard rate ~ 7% p.a. for eligible loans. |

| Interest Subvention to Banks | ~ 1.5% interest subsidy provided to eligible lending institutions. (Press Information Bureau) |

| Prompt Repayment Incentive (PRI) | Additional up to 3% interest reduction if repayment is timely, making effective rate for the farmer ~ 4%. |

| Coverage / Implementation | Scheduled Commercial Banks, Regional Rural Banks (RRBs), and Cooperative Banks operate this. The Reserve Bank of India (RBI) and National Bank for Agriculture and Rural Development (NABARD) are responsible for its implementation. They also monitor the process. |

| Digital/Operational Tool | Launch of the Kisan Rin Portal (KRP) in 2023 to track claims and enhance transparency. (Insights on India) |

| Calamity Relief Provision | For loans restructured due to natural calamities, additional subvention may be available (in earlier versions). |

4. Eligibility & Conditions

- The farmer must be availing a short-term agricultural loan (e.g., for crop production) via a KCC or approved credit route.

- The loan should be within the prescribed limit. The limit is ₹ 3 lakh for crop loans and up to ₹ 2 lakh for allied activities. This is necessary for subvention eligibility.

- Timely repayment yields the additional prompt repayment incentive.

- Lending institutions must be eligible and claim the subvention in accordance with scheme norms.

5. Implementation & Process Flow

- Farmers apply for KCC/short-term loan in bank/cooperative/eligible financial institution.

- Bank sanctions loan under KCC/short-term credit.

- Farmer receives funds at the subsidised interest rate (effectively 7% or possibly 4% if timely repayment).

- Lending institution receives subvention from Government (1.5%) for providing subsidised loan.

- Claims and reimbursements of subvention process via RBI/NABARD and digital portal (Kisan Rin Portal) for transparency and speed.

6. Key Data & Recent Developments

- As of FY 2025-26, the scheme has been continued with existing parameters (1.5% subvention) by the Cabinet.

- Over 7.75 crore KCC accounts are covered under the scheme. (Press Information Bureau)

- Institutional credit through KCC increased from ₹4.26 lakh crore in 2014 to over ₹10.05 lakh crore by December 2024. (Press Information Bureau)

7. Benefits / Significance

Makes credit for agriculture more affordable, thus reducing dependence on informal high-cost loans.

Encourages institutional credit flow to agriculture, supporting farms and allied activities.

Promotes financial inclusion of small and marginal farmers.

By incentivising prompt repayment, helps improve the credit discipline in the agricultural credit system.

Enhances overall rural economy by ensuring working capital availability for crop production, allied activities, and related costs

8. Challenges & Considerations

- Though the scheme reduces interest cost, access to credit still depends on bank branch reach, documentation, and farmer awareness.

- The upper loan limit (₹3 lakh) may not be sufficient for some higher-cost crops/allied enterprises in certain regions.

- While subvention supports the interest cost, other costs of production, input inflation, and climate risks still challenge farmers.

- Timely repayment incentive depends on proper tracking; default or delayed repayments still pose risk to both bank and farmer.

- Effective monitoring and speedy claim processing require robust digital systems and oversight.

9. Handbook “At a Glance” Table

| Item | Key Parameter |

|---|---|

| Scheme Name | Modified Interest Subvention Scheme (MISS) |

| Launch / Origin | Early interest-subvention schemes ~2006-07; modified version later. (IMPRI India) |

| Objective | Affordable short-term credit for farmers + allied activities |

| Loan Limit | ₹3 lakh for crop loans; up to ₹2 lakh for allied (as per current guideline) |

| Interest Rate to Farmer | ~7% (base) |

| Interest Subvention to Banks | ~1.5% |

| Prompt Repayment Incentive (PRI) | Up to 3% → Effective rate ~4% for farmers |

| Implementing Agents | SCBs, RRBs, Co-ops; monitored by RBI/NABARD |

| Digital Platform | Kisan Rin Portal (KRP) |

| Coverage | Millions of KCC accounts; agricultural credit increased significantly |

| State / UT | Number of KCC accounts benefitting under MISS* | Total credit disbursed under KCC (₹ crore) | Percentage of small/marginal farmers covered | Average interest rate to farmers (after PRI) | Additional state-specific incentives (if any) | Notes / Data source & Year |

|---|---|---|---|---|---|---|

| State A | ||||||

| State B | ||||||

| … | ||||||

| All India | ~7.75 crore KCC accounts (nationwide) (Press Information Bureau) | KCC credit ~ ₹10.05 lakh crore (by Dec 2024) | Effective rate ~4% for timely repayment |

10. Region-wise & State-Specific Implementation under MISS

Why implementation varies by state

MISS is a Central Sector Scheme – so the core rules are uniform across India (same subvention rate, same KCC loan cap etc.). What varies by state is:

- Scale of use of Kisan Credit Cards (KCC) – number of active cards and outstanding loan amounts.

- Additional state-level interest subvention – some states add extra subsidies on top of MISS. (ScienceDirect)

- Depth of cooperative / RRB networks – especially in states with strong cooperative banking.

- Crop pattern & irrigation – high-input irrigated states tend to use more KCC credit.

RBI’s Appendix Table IV.8 (Trend and Progress of Banking in India, 2022–23) gives a detailed state-wise snapshot of operative KCCs. It also provides information about outstanding amounts. This effectively shows the scale of MISS-linked credit in each state. (Reserve Bank of India)

Snapshot: Top states by KCC exposure (proxy for MISS reach)

(At end-March 2023 – “Total” column of all banks combined) (Reserve Bank of India)

| State | Approx. no. of operative KCCs (’000) | Approx. outstanding KCC loans (₹ crore) | Key Takeaways for MISS Implementation |

|---|---|---|---|

| Uttar Pradesh | ~10,700 | ~1,28,000 | Largest KCC portfolio in India. MISS is extremely significant here. Even small changes in subvention design impact millions of farmers. |

| Rajasthan | ~6,500 | ~99,500 | Very high cooperative & RRB presence; large use of KCC for dryland crops under MISS. |

| Madhya Pradesh | ~6,300 | ~78,000 | Strong uptake of KCC for wheat, soybean & pulses; MISS supports a big chunk of seasonal farm credit. |

| Maharashtra | ~7,200 | ~70,000 | High outstanding KCC loans; state also runs its own interest subvention scheme, further lowering effective interest for farmers beyond MISS. |

| Gujarat | ~3,000 | ~62,000 | Strong cooperative network; high KCC use for cotton, groundnut and horticulture. |

| Andhra Pradesh | ~4,550 | ~60,000 | Substantial MISS coverage, especially through RRBs and commercial banks for paddy and horticulture. |

| Karnataka | ~4,700 | ~54,000 | Heavy use for sugarcane, paddy, maize; both co-ops & SCBs are big conduits of MISS support. |

| Telangana | ~4,300 | ~44,000 | High KCC penetration; MISS dovetails with state schemes for paddy & cotton credit. |

| Kerala | ~2,600 | ~43,000 | Rapid jump in KCC outstanding between 2022–23; key for plantation & cash crops. |

| Tamil Nadu | ~3,600 | ~42,000 | High institutional credit for rice, sugarcane & horticulture; MISS is an important interest support. |

Note: These are rounded numbers derived from RBI’s state-wise KCC table and should be treated as indicative magnitudes, not exact audited figures. (Reserve Bank of India)

Region-wise implementation profile (RBI regional groupings)

RBI groups states into broad regions for KCC statistics, which gives a good lens on MISS reach. (Reserve Bank of India)

(a) Northern Region – Haryana, Punjab, Rajasthan, Himachal Pradesh, J&K, etc.

- KCC footprint: High – particularly in Rajasthan, Punjab and Haryana, with strong cooperative and RRB presence.

- Usage pattern:

- Punjab & Haryana: intensive, irrigated wheat–paddy systems; KCC loans under MISS are crucial for seed, fertilizer, diesel.

- Rajasthan: large number of operative KCCs for dryland crops (bajra, mustard, gram).

- State extras:

- Haryana historically provided very high interest relief; under earlier policies farmers effectively paid near-zero interest in some years, which is why changes to MISS interest terms are politically sensitive there.

Implementation highlight:

Northern states show high per-farmer loan sizes and strong linkage of MISS with cooperative banks and PACS, especially for wheat–paddy and oilseeds.

(b) Western Region – Maharashtra, Gujarat, Goa, DNH & Daman & Diu

- KCC footprint: Very large, with Maharashtra and Gujarat among the top KCC users nationally. (Reserve Bank of India)

- Usage pattern:

- Maharashtra: sugarcane, cotton, soybean; heavy reliance on short-term crop loans.

- Gujarat: cotton, groundnut, horticulture; significant KCC-linked credit in Saurashtra and North Gujarat.

- State extras:

- Maharashtra operates a state-level interest subvention scheme to bring crop loan rates near 6% or even lower for prompt payers, over and above MISS.

Implementation highlight:

Western states are credit-intensive – high outstanding per card plus additional state support makes the effective interest burden relatively lower for many farmers.

(c) Central Region – Uttar Pradesh, Madhya Pradesh, Chhattisgarh, Uttarakhand

- KCC footprint:

- UP and MP form the core of India’s KCC universe. They have the single largest outstanding KCC credit pool in the country. (Reserve Bank of India)

- Usage pattern:

- UP: highly diversified – paddy, wheat, sugarcane, vegetables.

- MP & Chhattisgarh: wheat, soybean, rice; significant share of KCC loans for input purchases and seasonal labour.

- Implementation note:

- The sheer number of small & marginal farmers contributes to this impact. Any change in MISS parameters here has a national-scale impact on farm finances.

Implementation highlight:

Central India is the heartland of MISS. It accounts for a huge share of KCC accounts and outstanding loans. This is especially true through scheduled commercial banks.

(d) Southern Region – Karnataka, Kerala, Andhra Pradesh, Tamil Nadu, Telangana, Puducherry, Lakshadweep

- KCC footprint: Very high, with rapid growth in outstanding amounts between 2022 and 2023. (Reserve Bank of India)

- Usage pattern:

- Karnataka: sugarcane, paddy, maize, arecanut.

- Andhra Pradesh & Telangana: paddy, cotton, chillies; high credit dependence for canal & borewell irrigation systems.

- Tamil Nadu & Kerala: rice plus plantation/horticultural crops (coconut, rubber, spices).

- State extras:

- Several southern states supplement central schemes with their own interest rebate programs. They also have loan waiver histories, which influence repayment culture. This affects the demand for MISS-subsidised credit.

Implementation highlight:

Southern region shows strong integration of MISS with PACS. It also demonstrates cooperative structures and high usage for intensive horticulture. These are evident in the production of cash crops.

(e) Eastern Region – Odisha, West Bengal, Bihar, Jharkhand, Andaman & Nicobar

- KCC footprint: Moderate-to-high, with substantial numbers in Odisha, West Bengal and Bihar. (Reserve Bank of India)

- Usage pattern:

- Odisha: paddy-centric with rainfed and irrigated pockets.

- West Bengal: smallholder-dominated paddy, jute, potato; KCC is key for seasonal working capital.

- Bihar & Jharkhand: growing but still relatively under-served compared to potential – institutional credit penetration is improving.

- Implementation note:

- Scope for expansion of MISS reach remains significant. This can be achieved by strengthening RRBs and PACS networks. Additionally, pushing KCC coverage in flood- and drought-prone districts will be beneficial.

Implementation highlight:

Eastern India is a focus area for deepening KCC/MISS penetration, given high rural population and many small-holder farmers.

(f) North-Eastern Region – Assam, Meghalaya, Manipur, Mizoram, Nagaland, Tripura, Arunachal Pradesh, Sikkim

- KCC footprint: Overall low in absolute numbers, but growing, especially in Assam, Meghalaya and Tripura. (Reserve Bank of India)

- Usage pattern:

- Dominated by small and fragmented holdings with horticulture, paddy and plantation crops.

- Access issues (terrain, sparse bank branches) affect uptake.

- Implementation note:

- MISS here is tightly linked with broader financial inclusion and KCC expansion drives; Kisan Rin Portal and PACS digitisation are particularly important in this region.

Implementation highlight:

North-East is more about building the pipeline – expanding KCC coverage so that MISS benefits can reach a larger share of farmers.

Role of state-level top-ups with MISS

Beyond the central 1.5% interest subvention + up to 3% prompt repayment incentive under MISS, several states implement their own interest subvention schemes. This ensures that effective interest rates in some states drop to 0–4% for timely payers.

Typical patterns:

- Maharashtra: explicit state scheme giving banks an extra subvention so crop loans can be given at around 6% or lower. (mahasahakar.maharashtra.gov.in)

- Some northern states (e.g., Haryana earlier): political push for near-zero effective interest on crop loans, either through top-ups or waivers.

MISS is often the “base layer”. State governments decide how much further relief to give on top of it.

11. Conclusion

The Modified Interest Subvention Scheme (MISS) plays an important role in India’s agricultural credit system. MISS reduces the cost of short-term loans. It also provides incentives for prompt repayment. This helps farmers access institutional credit in a timely, affordable manner. This in turn supports farm production, allied activities (such as animal husbandry and fisheries), and rural livelihood security.

While the scheme is well-designed and broadly impactful, its true value lies in effective implementation. It ensures that eligible farmers know about it. Banking institutions promptly extend loans. Documentation is streamlined. Benefits flow without delay. Digital systems like the Kisan Rin Portal function smoothly.

For India to realise its goals of doubling farm income and strengthening agro-rural growth, schemes like MISS must continue evolving. They need to address issues such as higher credit limits, broader coverage, and better awareness. Additionally, integration with other agricultural support measures is crucial.

In essence: Affordable credit + timely repayment + institutional discipline = stronger agricultural growth. MISS encapsulates this formula and remains a cornerstone of India’s farm-credit policy.

Leave a comment